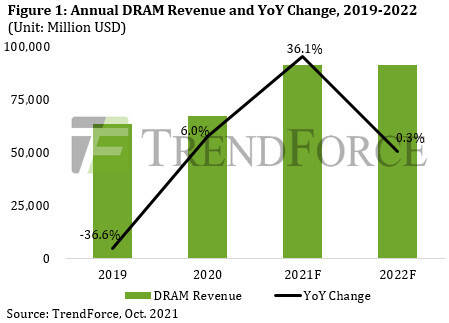

DRAM contract prices are likely to exit a bullish period that lasted three quarters and be on the downswing in 4Q21 at a QoQ decline of 3-8%, according to TrendForce’s latest investigations. This decline can be attributed to not only the declining procurement activities of DRAM buyers going forward, but also the drop in DRAM spot prices ahead of contract prices. While the buying and selling sides attempt to gain the advantage in future transactions, the DRAM market’s movement in 2022 will primarily be determined by suppliers’ capacity expansion strategies in conjunction with potential growths in demand. The capacity expansion plans of the three largest DRAM suppliers (Samsung, SK hynix, and Micron) for 2022 are expected to remain conservative, resulting in a 17.9% growth in total DRAM bit supply next year. On the demand side, inventory levels at the moment are relatively high. Hence, DRAM bit demand is expected to grow by 16.3% next year and lag behind bit supply growth. TrendForce therefore forecasts a shift in the DRAM market next year from shortage to surplus.